As the Covid-19 pandemic ushers in another era of ultra-low interest rates, Rathbone’s Bryn Jones has been favouring banking and insurance bonds in an environment where credit risk and duration risk continues to grow.

While some investors might not consider the banks to be among the issuers to be found in an ethical bond strategy – particularly after payment protection insurance (PPI) scandals and the outsized role they played in the global financial crisis – Jones said they, along with insurers have a compelling argument for being included.

“A lot of people criticise banks and insurance companies, but without banks and insurance companies there’d be pretty much anarchy, they are social investment to a certain extent,” said Jones.

The manager of the £1.6bn Rathbone Ethical Bond fund said he likes the banking sector because “over the last 10 years they’ve cleaned up their balance sheet and they’ve deleveraged”.

Jones said, “as an active manager if we don’t like sectors we won’t invest, if we like sectors we will invest with conviction”.

Indeed, the fund has just under three-quarters of its capital invested in banking and insurance bonds.

He highlights the fact that Nationwide’s Tier-1 capital ratio has grown from around 15 per cent in 2010, to above 30 per cent today, and that this trend has been going on globally in the sector.

“Regulators force big banks to have additional Tier-1 capital so should we have another 2008 global financial crisis-style event, there’s a bit of cushion for more senior investors,” he said.

“None of this capital is going to be able to be used for regulatory capital beyond 2021, so they’re going to have to call these bonds or tender them because it’s very expensive form of capital.

“Beyond 2021 the regulators won’t be able to recognise certain previously issued Tier-1 debt as Tier-1 capital, and the banks can’t use it as capital, therefore it becomes very expensive,” he explained, noting that Lloyds has a 13 per cent coupon on one of its Tier-1 bonds.

“We think they’re going to take these bonds out, and when they do there’s a significant capital uplift for us. There’s a make-whole provision in the covenants which means they have to take them out at very tight spreads,” Jones said. “When they come to market with a tender request, you’re up 10, perhaps, 15 per cent capital uplift overnight in the asset price.

“So, we’ve made a very large position with very high conviction, lots of alpha waiting to come through when that happens.”

He added: “You're looking at double-digit yields which for investment grade sterling investor is quite incredible.

“If you think the 10-year gilt is currently yielding you less than 0.2 per cent, and if you get 10 per cent return from these assets that significant.”

The other part of his conviction in the financial sector focuses on insurers where he has also found interesting opportunities.

“Insurers have been able to get through a credit crisis, a sovereign debt crisis, Solvency 2 requirements, Covid-19: they’ve been fairly resilient, strong solvency businesses. Again, it’s another area where you look at the risk-adjusted returns you can achieve in insurance, they’re really attractive.”

The manager of the Rathbone Ethical Bond fund said he has spent more time looking at which banks are sustainable as an ongoing project, given that the strategy was launched 18 years ago before the UN Sustainable Development Goals – a key benchmark for many ethical strategies – existed.

“Now we’ve got climate change and at the moment we’re evolving our process to take into consideration more sustainable ideas on top of the ethical screening that we do,” he explained.

While green bonds are relatively large and prevalent in Europe, Jones said, “you have to take it with a bit of a pinch of salt”: if the bonds breach their fund’s negative screening criteria, they can’t buy it.

He drew an example to the Norwegian oil tanker firm Teekay Shuttle Tankers that recently issued a green bond; “they were using more energy efficient ships but they were shipping oil about, so you have to take it security by security”.

Some bonds he has been picking up lately have been the Covid-19 response bonds, which he said came from very high quality AAA issuers, such as the European Bank for Reconstruction and Development and the African Development Bank.

“We’ve invested in those because of those are the economies which struggle in their response to the risks of Covid-19,” he explained.

However, while the fund hasn’t invested in all of the Covid-19 response bonds, they are generally very high quality and aligned with the objective of the Rathbone Ethical Bond fund which is to invest into social purposes.

The fund also has about 2 per cent invested into small bonds where it can have a big impact, such as Burnham and Weston, one of the largest community solar farms in the UK, and Linton Hydro, a hydroelectric power scheme in north Yorkshire.

“These business are generating very tidy yields, but it has a big impact,” Jones said.

Another recent challenge has been compounding income, as credit quality has deteriorated not only because debt issuance is likely to increase, but also because earnings have collapsed as a result of the Covid-19 crisis. This is in combination with the duration risk that Jones highlights as significantly higher than in previous years due to the low interest rates investors are facing today.

He said that in 1996 an investor got an 8 per cent yield for a five-year duration bond, which meant that for every 1 per cent rise in yields would lead to a 5 per cent fall, but an investor would still get an 8 per cent income.

“In 1996 you could have made 3 per cent quite easily from investing in a bond portfolio. You could’ve really messed it up, got all the credits wrong, spreads could’ve widened, but you got an 8 per cent yield, happy days, you still would’ve made a 3 per cent return.”

The current yield for the sterling corporate bond index is about 1 per cent , with nearly a nine-year duration.

“What you get is this situation where you’re only yielding 1 per cent, and the duration is 9,” he said. “So, a 1 per cent rise in yields would give you a negative return of 9 per cent, and you’ll only get 1 per cent income, so you make negative 8 per cent.”

“If you make a complete pigs ear of your portfolio now, you can lose 8 per cent, but in 1996 you’re making 3 per cent, a 11 per cent differential.”

As a result Jones anticipates a lot of volatility between different fixed income funds going forward.

Jones has managed the Rathbone Ethical Bond fund since 2004, latterly alongside Noelle Cazalis.

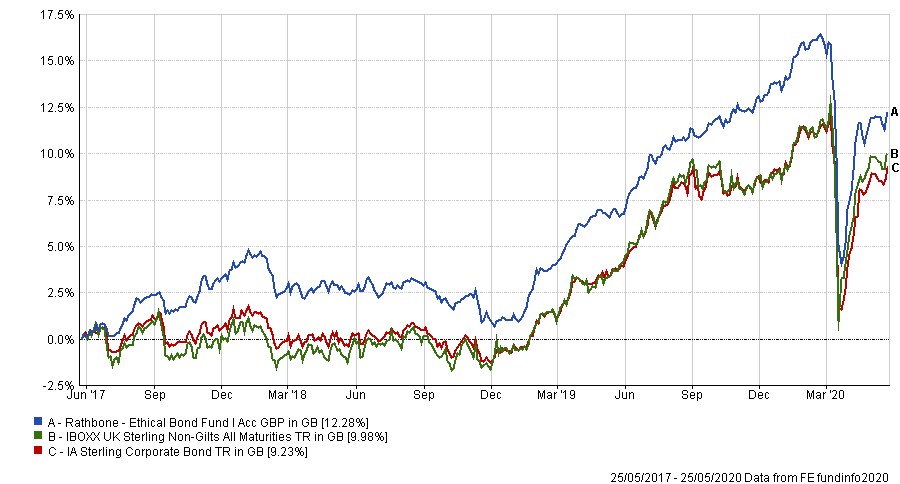

Performance of fund vs sector & benchmark over 3yrs

Source: FE Analytics

Over the past three years the five FE fundinfo Crown-rated fund has made a total return of 12.28 per cent compared with a 9.98 per cent gain for the IBOXX UK Sterling Non-Gilts All Maturities benchmark and a 9.23 per cent return for the average IA Sterling Corporate Bond peer. It has a yield of 3.7 per cent and an ongoing charges figure (OCF) of 0.66 per cent.