Asian equities offer better growth potential than the US market, according to Jason Day, senior investment manager at abrdn, who has cut exposure to US equities across his five portfolios in favour of Asia, Japan and the emerging markets.

High inflation and tightening monetary policy have fundamentally altered how markets work, hence the need for a reassessment of the investment strategy, according to Day, who repositioned his portfolios in March.

Overall, the average allocation to Asia and emerging markets across the portfolios rose from 12% to 21%, while exposure to US equities was cut from 25% to 23% on average across the five portfolios, which each have varying levels of risk.

The highest-risk portfolio had its allocations to US equities cut by 4.7 percentage points to 38.6%, while exposure to Asian and emerging market equities rose 7.4 percentage points to 18.5%.

Day said: “Fundamentally, it came down to where do we thought future growth was going to come from. Asia ticks all the boxes for us.”

The US has been a crucial market for growth investors in the past but Day said it may not be sustainable, pointing out that just eight companies drove 60% of the S&P 500’s performance over the past decade.

“Tech is still going to be important, but I find it hard to believe that those eight companies are going to drive outperformance over the next decade,” Day added. “You’re going to get a wider dispersion of returns in the US, so we think it's a good time to trim it back.”

Despite a widespread fall in share prices across US equities last year, they are still too overpriced, according to Day.

The average stock in the US market is trading at 22x earnings, the same level they were at before the recent downturn, which is expensive.

Day said: “The majority of economists expect a recession this year yet US equities are trading at a premium. That’s going to hit corporate profitability and put them under pressure.”

Asian and emerging market equities, on the other hand, are trading at 12x earnings on average while also being “well positioned to benefit from that environment”.

Companies in the region have had a tough few years, especially in China after common prosperity and zero-Covid measures repelled investment, but market conditions have become more corporate-friendly, according to Day.

He said: “The government has been very proactive in making the listing rules easier, so that opportunity set is growing and becoming more attractive to foreign investors.”

Day increased exposure to the region through a blend of growth and value funds such as Schroder Asian Income and Fidelity Asia.

He said Fidelity Asia doesn’t invest in Australasia or Asia-Pacific companies, giving it raw exposure to high-growth opportunities in mainland and emerging Asia.

This is balanced out with Schroder Asian Income, which holds “well established companies that have lower risk,” according to Day.

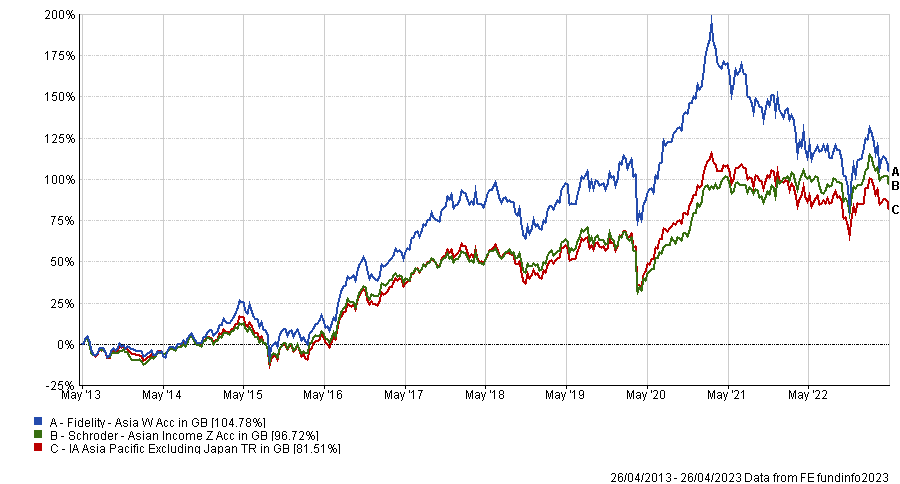

The Fidelity and Schroder fund were up 104.8% and 96.7% respectively over the past decade, beating the IA Asia Pacific Excluding Japan sector’s total return of 81.5%.

Total return of funds vs sector over the past 10 years

Source: FE Analytics

These two funds were already holdings in the portfolios before the reshuffle, but Day added FSSA Asia Focus for extra growth exposure.

He said: “It does have growth on its skyline but there's more quality in that portfolio, so that's quite a good mitigator when combined with Fidelity Asia. There's a different mindset between the two teams.”

For exposure to emerging markets, Day increased allocations to the Artemis SmartGARP Global Emerging Markets Equity fund.

The value-oriented fund has beaten the IA Global Emerging Markets sector by 31.7 percentage points since launching in 2015, climbing 65.2%, but Day said it can go through periods of turbulence.

“There have been periods where China tech has dominated emerging market forces – think Baidu, Alibaba and Tencent – where it’s been very much behind,” he said. “Although it's interesting because it has been buying into those companies now that they've sold off so heavily.”

Its growth-heavy partner is Redwheel Global Emerging Markets, which is up 99.9% since it went live in 2016. Day said: “It’s high active share and very much benchmark agnostic, which makes it a very good long-term holding. Performance can be a little bit bumpy over the short term, but we think it's a really great strategy to have longer term.”

Asia and emerging markets may have overtaken the US in Day’s portfolios, but UK exposure remained the same.

He took it “down to the bare bones” last year at 27.7%, and while it hasn’t gone any lower, challenges still lie ahead in how the UK contends with its faster-growing neighbours.

Day said: “The UK is very much an old economy that has held up really well year-to-date despite being a bit choppy with those tremors in the banking system.

“It's very value oriented, which is a nice offset from the US, but the challenge would be its growth prospects. That’s going to be a bit of a bit of a headwind, so the UK stock market is a bit challenged.”

Fixed income also became a bigger theme in Day’s portfolios after an “exceptionally difficult” period in 2022. He said: “Like a phoenix rising from the ashes, the starting point now is particularly attractive for a lot of fixed income segments.

“Whilst the overall return over the long term might not be as strong as equities, fixed income is the most attractive asset class for risk adjusted returns.”

Average fixed income exposure lifted 2 percentage points from 28.9% to 31.1% across the five portfolios, with global index linked bonds and global investment grade bonds getting the biggest uplifts. Despite poor performance last year, he also increased exposure to US investment grade bonds because “they’ve got a really good risk profile again”.